Gil datner-anaylist bank Leumi

21/05/2015

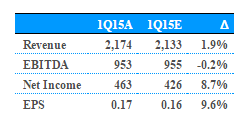

Bezeq reported 1Q15 results in line with expectations though better on the bottom line on lower than expected finance and tax costs.

Fixed line.

Telephony earnings were relatively stable on a small increase in subs and a 4.7% decrease in ARPL (lower than the rate in 2014). Broadband continued to perform well adding 26k subs (similar to 2014 run rate), while ARPU actually increased an impressive 6.1%. The company reported on 11k wholesale subs. Revenue from transmission continued to grow consistently. Costs not including D&A were relatively unchanged.

The picture in the fixed line segment will not remain static as competition increases through a developing wholesale market, the IEC's FTTH infrastructure, and Hot's improving service levels. These elements will take time to be felt, particularly after the removal of the MoC's director. However the trend of increasing competition appears well established.

Wireless

Subs declined 21k vs. ~63k for PTNR and 82k for CEL. ARPU declined a hefty 18.8% YoY on tougher price competition and the loss of ILS 52m hosting revenues from Hot Mobile (which will establish a shared network with PTNR). Equipment sales came in at ILS 228m, 5.8% down on the 2014 quarterly average. Costs came down on a voluntary retirement plan concluded at the end of 2014. As a result of the relatively low churn, cost reductions and lower equipment sales, operating cash flow remained healthy at ILS 351m, unchanged YoY.

Pelephone is coping well but it is in a difficult situation. As the only company without a network sharing agreement, it faces an inherent cost disadvantage in an industry where the has shifted decisively to a low cost business model.

ISP/ILD

The picture remained stable – higher revenues YoY offset by higher costs, with EBITDA up 3.2%.

PayTV.

We are seeing some pressure on sub numbers, ARPU and costs on the increased competition, resulting in a 5% YoY decline in EBITDA.

Bottom line. The telecom market is not changing as fast as had been expected due to constant delays in regulation, and the slow progress of Unlimited (the Israel Electric Corporation's FTTH venture). However, it is changing and will continue to do so, with the focus being on increased competition in services delivered through the fixed line network. We think Bezeq's current valuation does not reflect the risks inherent in the changing competitive environment. We are currently at Underperform with a ILS 5.7 (adjusted for the recent dividend), which is 15% below the market price.

Important Disclosures:

Important Information for readers in the US

Leumi Investment Services Inc. (LISI) accepts responsibility in the U.S. for the content of this research report prepared by its non-US affiliate, Bank Leumi Ie-Israel B.M. (Bank Leumi). U.S. persons—other than U.S.-registered broker-dealers and U.S.-regulated banks—receiving and/or accessing this report and wishing to effect transactions in any security discussed herein should do so with LISI in the United States.

The view(s) expressed in this Research Report accurately reflect the analyst(s)’ personal view(s)

The research analysts responsible for the preparation of this report receive compensation based upon various factors, including the quality and accuracy of research, client feedback, competitive factors, and overall firm revenues.

Bank Leumi Le Israel BM does not trade as principal in the securities or derivatives of the issuers that are the subject of this report.

Bank Leumi Le Israel BM does not have significant holdings in the securities mentioned in this report.

Bank Leumi Le Israel BM does not act as a market maker or liquidity provider in the securities of the subject issuer(s) mentioned in this report.

Bank Leumi Le Israel BM has not had an investment banking services client relationship during the past 12 months with the issuer(s) mentioned in this report.

Bank Leumi Le Israel BM has not had a non-investment banking services client relationship during the past 12 months with the issuer(s) mentioned in this report.

הנתונים, המידע, הדעות והתחזיות המתפרסמות באתר זה מסופקים כשרות לגולשים. אין לראות בהם המלצה או תחליף לשיקול דעתו העצמאי של הקורא, או הצעה או שיווק השקעות או ייעוץ השקעות ב: קרנות נאמנות, תעודות סל, קופות גמל, קרנות פנסיה, קרנות השתלמות או כל נייר ערך אחר או נדל"ן– בין באופן כללי ובין בהתחשב בנתונים ובצרכים המיוחדים של כל קורא – לרכישה ו/או ביצוע השקעות ו/או פעולות או עסקאות כלשהן. במידע עלולות ליפול טעויות ועשויים לחול בו שינויי שוק ושינויים אחרים. כמו כן עלולות להתגלות סטיות בין התחזיות המובאות בסקירה זו לתוצאות בפועל. לכותב עשוי להיות עניין אישי במאמר זה, לרבות החזקה ו/או ביצוע עסקה עבור עצמו ו/או עבור אחרים בניירות ערך ו/או במוצרים פיננסיים אחרים הנזכרים במסמך זה. הכותב עשוי להימצא בניגוד עניינים. פאנדר אינה מתחייבת להודיע לקוראים בדרך כלשהי על שינויים כאמור, מראש או בדיעבד. פאנדר לא תהיה אחראית בכל צורה שהיא לנזק או הפסד שיגרמו משימוש במאמר/ראיון זה, אם יגרמו, ואינה מתחייבת כי שימוש במידע זה עשוי ליצור רווחים בידי המשתמש.