- תוצאות תפעוליות חזקות, עם צמיחה בקניונים ובמשרדים

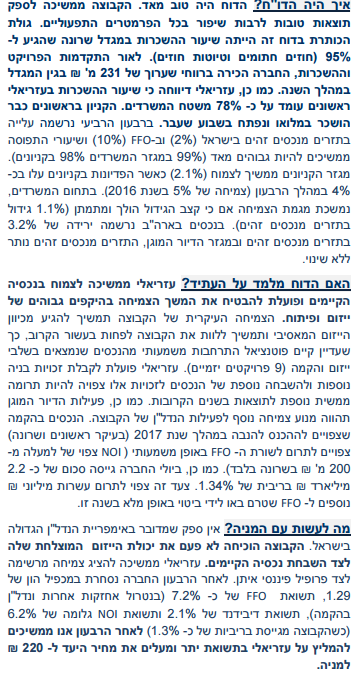

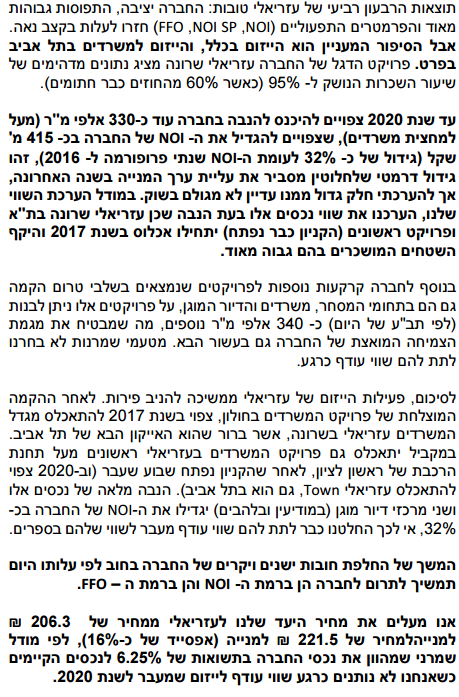

עזריאלי הציגה תוצאות תפעוליות חזקות, עם כ-5% צמיחה ב-NOI לכ-338 מיל' ₪ מעל לציפיות, כתוצאה מצמיחה חזקה של כ-4% בתחום הקניונים וצמיחה מתונה של כ-1% בתחום המשרדי בישראל. החברה ממשיכה ליהנות מחיסכון בהוצאות מימון כתוצאה ממחזור חוב, שתמשיך להשפיע ברבעון הראשון. למרות העלייה בהוצאות שיווק, עזריאלי הציגה כ-10% צמיחה ב-4Q16 לכ-244 מיל' ₪ לעומת 4Q15 כתוצאה מהצמיחה במגזר הקניונים וחיסכון בהוצאות מימון.

- צמיחה יציבה בתחום הקניונים, ה-NOI ברבעון צמח לכ-200 מיל' ₪

עזריאלי דיווחה על צמיחה נאה של כ-4% ב-NOI לכ-200 מיל ₪, כשרוב הצמיחה נובעת מרכישת מתחם מסחרי ברעננה. על בסיס נכסים זהים, עזריאלי דיווחה על צמיחה של כ-2% ב-NOI, מעל הצמיחה של כ-1% ב-Q3. אנו אופטימיים לגבי תחום הקניונים, כתוצאה מנתוני צריכה פרטית חזקים (+4.9% בחציון השני) כשאנחנו מעריכים שנתונים אלו ימשיכו להשתקף בצמיחה בפדיון שוכרים (+4% ברבעון הרביעי) בעתיד. נתונים אלו הורידו את עומס השוכרים מ-11.9% בשנת 2015 לכ-11.3%בשנת 2016 ותתמוך בעדכון כלפי מעלה של שכ"ד בעתיד.

- צמיחה מתונה יותר בתחום המשרדים בישראל לאור תחלופה נמוכה של דיירים

עזריאלי רשמה צמיחה מתונה יותר של כ-1% לכ-95 מיל' ₪ בתחום המשרדים. למרות הגידול המרשים בשכ"ד בגין חוזים חדשים (כ-21% גידול בת"א וכ-6% בהרצליה), ההשפעה על צמיחת ה-NOI הייתה שולית לאור התחלופה הנמוכה של דיירים ברבעון. הגידול המרשים בשכ"ד בת"א (כולל כ-12% גידול בעדכון חוזים קיימים) מרמז על ביקוש איתן ל-Class A נכסים בת"א ומפחית את הסיכון בפרויקט שרונה (השקה ב-4Q17, שעור ההשכרות מחוזים חתומים ובשלבי חתימה עומד על 95%).

- צורכי מימון מינימליים מהווים יתרון בסביבה הנוכחית

כתוצאה מגיוס חוב של כ-2.2 מיליארד ₪ ביולי 2016, הריבית הממוצע ירדה לכ-2.05% בשנת 2016 לעומת כ-2.44% ב-2015. אנו צופים עוד ירידה משמעותית בהוצאות מימון ב-Q1 כתוצאה ממחזור חוב יקר הנושא ריבית של כ-5%. אנו עדים לסביבת ריבית נוחה יותר ב-Q1, המשתקף בירידה של כ-31 נ.ב. לכ-1.6% (אג"ח ד) מרמות שיא של סוף 2016. אנו מציינים את המרווח הגדול היחסי והאטרקטיבי של כ-440 נ.ב. בין implied cap rate לתשואת האג"ח לעומת כ-90 מרווח ל-US reit's.

- צמיחה חזקה ב-FFO, פרויקטי ייזום ישפיעו באופן מהותי על 2017 ו-2018

למרות העלייה בהוצאות תפעול (בעיקר שיווק) ברבעון, ה-FFO צמח בכ-10% לכ-244 מיל' ₪ לעומת 15Q4 כתוצאה מחיסכון בהוצאת מימון. אנו מתרשמים מתוכנית הייזום, ולהערכתנו, פרויקט ראשונים ושרונה יתרמו 65 ₪ ל-NOI ב-2017 ועיקר ההשפעה – כ-175 מיל' נוסף ב בשנת 2018. אנו צופים צמיחה של כ-7% לכ-1.02 מיליארד ₪ ב-FFO בשנת 2017 וכ-15% צמיחה לכ-1.17 מיליארד ₪ בשנת 2018.

- תמחור: מעלים את מ"י ל-223 ₪ בזכות סביבה תפעולית חזקה, ממשיכים להמליץ בקניה

אנו מתרשמים מהשילוב של פרויקט ייזום שישפיעו על צמיחת ה-FFO בשנת 2017-2018 ומינוף הנמוך (31% LTV). לאור ציפיותינו להמשך סביבה תפעולית טובה (שכ"ד בתחום הקניונים והמשרדים) ושני פרויקטי נדל"ן שיתחילו להניב ב-2017 וסביבת ריבית נוחה העלנו את מכפיל ה-FFO על נכסים מניבים מ-x16.7 ל-x18.2 (תשואת של 5.5%) ומחיר היעד מ-205 ל-223, המשקף אפסייד של כ-12% למחיר המניה בשוק.

דוד גבאי, אנליסט הנדל"ן של אקסלנס ברוקראז', ממשיך להמליץ קנייה של מניית קבוצת עזריאלי

ברורית פיין אנליסטית בלידר שוקי הון לדוחות עזריאלי

אנליסט – שי ליפמן אנליסט VALUE BASE

Main metrics in line, raising DPS by 20%

Azrieli reported a solid set of FY 16 results, led by NIS 533m of portfolio revaluation:

real Estate FFO is up 9% y-o-y to NIS 948m (UBSe: NIS 946m), Israel LFL NOI up 3% and EPRA NAV p.s. up 8% y-o-y to NIS 149 (UBSe: NIS 151). The company is raising DPS by 20% to NIS 3.96, in excess of our estimate (UBSe: NIS 3.59) demonstrating a confident outlook. We note DPS has doubled since IPO in 2010. Last week, we note reiterating our Buy rating (link: Still constructive on the Israeli real estate sector), driven by our positive view on:

-

the Israeli economic outlook

-

a prime portfolio and experienced management team with a track-record of utperforming; and

3) revaluation potential from both an attractive development pipeline and high-yielding property portfolio. Operations screen well, 99% average occupancy Occupancy rates remain high, both in both Israel malls (98%) and office (99%). In malls, we note that Rishonim Mall was opened just a few days ago, fully leased-up and including the first Israeli stores of SuperDry, Foot Locker and H&M Home. Across the mall portfolio, turnover rose by a healthy 5% y-o-y, leading to an undemanding 11.3% rent-to-revenue ratio, hence offering room for future rental growth. In office, revenues increased by 6% as the company is benefiting from strong demand for modern office space. In Azrieli Towers, new contracts were signed with an average increase of 21% (NIS 126 per sqm per month) compared with the average monthly rent for the property (NIS 104).

10% yield on pipeline, more leasing progress at Sarona Projects under construction are still guided to deliver an attractive yield of 10%. Further progress was made in leasing up Sarona with 95% of the leasable office space under signed contracts and drafts in signing stages. During and after the quarter 8,500 sqm were leased. In our view, with a net financial debt to assets ratio of just 26%, the company looks in solid financial shape to fund its large, attractive development pipeline. Valuation: trades at a 24% prem. to spot NAV (vs. 2% disc. for Pan-Europe) Our PT is based on our economic profit method, with a 10.1% ROIC and 6.0% WACC.

Valuation Method and Risk Statement

-

Slowdown in the growth of consumer spending in Israel;

-

Inflationary and interest rate risk: part of the group's debt is linked to CPI, fluctuating CPI has

-

impact on company’s financing expenses and hence cash flow projections;

-

The Group's non property interests may add additional volatility to NAV;

-

The Group has significant development exposure, which brings with it planning, construction, financing and letting risks; and

5) Potential over supply risk in the Tel Aviv office market. Our PT is based on our economic profit method with a ROIC of 10.1%

and a WACC of 6.0%.

Charles Boissier, CFA, Analyst UBS

Osmaan Malik, CFA, Analyst UBS

Data, information, opinions and forecasts which are published in these site suppliers surfers. Not be seen as a recommendation or a substitute for the independent judgment of the reader, or an offer or investment marketing or investment advice in mutual funds, ETFs, provident funds, pension funds, education funds or any other security or Real estate- between general and considering the special circumstances and needs of each call - the purchase and / or investments and / or activities or transactions whatsoever. The information may contain errors and may apply at market changes and other changes. In addition there may be variances between the forecasts presented in this review actual result. Writer may be a personal interest in this article, including the possession and / or making a deal for himself and / or for other securities and / or other financial products referred to in this document. The author may be a conflict of interest. Funder does not undertake to inform readers in some way such changes in advance or In retrospect. Funder shall not be liable in any way loss or damage incurred from using article / interview, if any, and does not guarantee that the use of this information may generate profits by the user.